How to Manage Personal Finances Book: Chapter 5- Creating a Monthly Budget

Author’s Note:

I am posting a text version of this entire book on Substack, and video versions on YouTube. Email ken@stltest.net for details on the book’s publishing date in late ’24 or early ’25.

**************************************************

The only reliable way to fund a savings account is to create a monthly budget and stick to your budgeting plan. That way, you’ll find ways to save money and budget for a savings amount each month.

You’ll save, because saving money is in your budget.

It’s time to introduce you to Sally, who you will get to know throughout the book. Here’s how Sally creates her monthly budget:

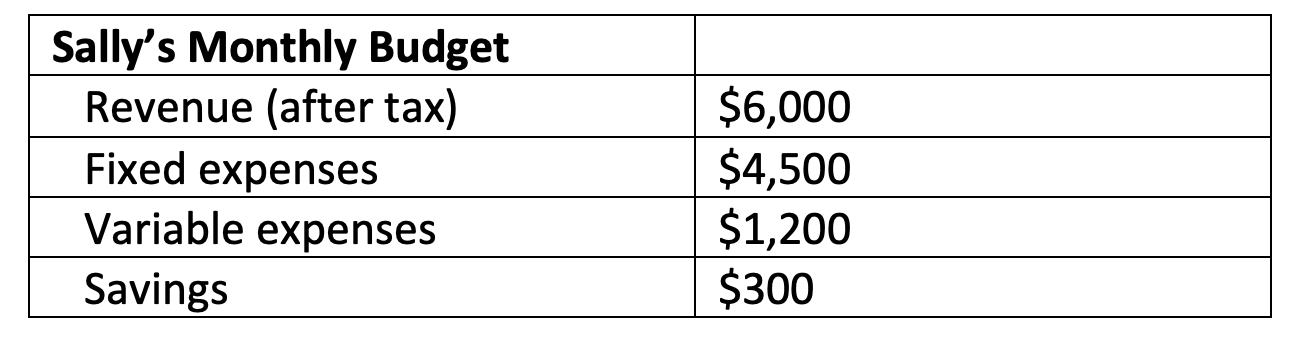

Setting up a budget template: Sally takes a blank piece of paper and writes her $6,000 after-tax monthly income (call it Revenue) at the top of the page. She also writes down categories for Fixed Expenses, Variable Expenses, and Savings.

Fixed expenses: Think about the fixed expenses you have every month. That will likely include your home mortgage, car payments, and insurance premium payments. Assume that Sally’s fixed expenses add up to $4,500.

Variable expenses: You now fit your variable expenses and your savings into the remaining $1,500 each month. Variable expenses are the ones you have some control over. Maybe rather than eat out three times a month, you only go twice. Or another one- you brew coffee a home three days a week, rather than buying from Starbucks. Sally’s variable expenses total $1,200.

Savings account: Your budget should include a monthly amount for savings. The first thing you do each month is pull out your budgeted savings amount and move it into a separate bank account. That way you don’t spend it. As an example, 5% of monthly gross income of $6,000 would be a savings amount of $300.

Here’s the budget:

There are lots of mobile apps to create and manage a monthly budget. The key is to plan your spending and review where you are a few times a month — regardless of what tool you use.

The benefit of saving sooner, rather than later

“Actually, I’ve always lived frugally and saved a lot of my income, so I don’t need to work for a while”

Wow.

It was 1999, and I was talking to a co-worker, Ron, who was about 50 years old. A large insurance company we both worked for was merging with another firm, and we were both leaving the company. (I’ve worked on my own since that job).

I had suspected that Ron lived well below his means, because I had a good idea of how much money he made. Both Ron and his wife worked, yet they lived in a blue collar-type neighborhood with small homes.

Ron wasn’t retiring early, but he had enough money to take some time off. He told me that he and his wife had planned financially, so neither of them would need to start working immediately after leaving a job.

They planned, they saved aggressively, and invested wisely.

This strategy can build wealth- even in times of market volatility.

The importance of an emergency fund

When you build and maintain an emergency fund, you can avoid borrowing money to pay for unexpected costs. Here are two common expenses that need to be funded:

Car repairs: In most places, you need a reliable car to get to and from work. Many people started working hybrid jobs during the pandemic and still need to go into the office a few days a week. A car repair can’t be put off.

Insurance copayments: Most of us pay a portion of the bill for medications, doctor visits, and other medical costs. An illness or injury is usually unplanned, and so is the cost of copayments.

When you build an emergency fund, you’ll have far less anxiety when unexpected costs come up. A car repair or copayment is frustrating, but having a fund to cover the cost reduces your stress level.

I’ll talk about the importance of insurance later.

The dollars you use to fund a savings/ emergency fund can’t be used for some other purpose. This is a good time to talk about opportunity costs (which is the next chapter)